India’s Green Manufacturing Gamble: Who Wins, Who Burns?

Scale ≠ Sustainable

India’s manufacturing sector already contributes 17% of GDP and employs nearly 60 million people. By 2030, it’s expected to touch $1 trillion.

But here’s the contradiction nobody wants to admit: Factories are chasing scale and speed, while climate reality demands slowness and redesign.

The result? A dangerous middle ground: India can grow big without going green, but it won’t grow global without going green.

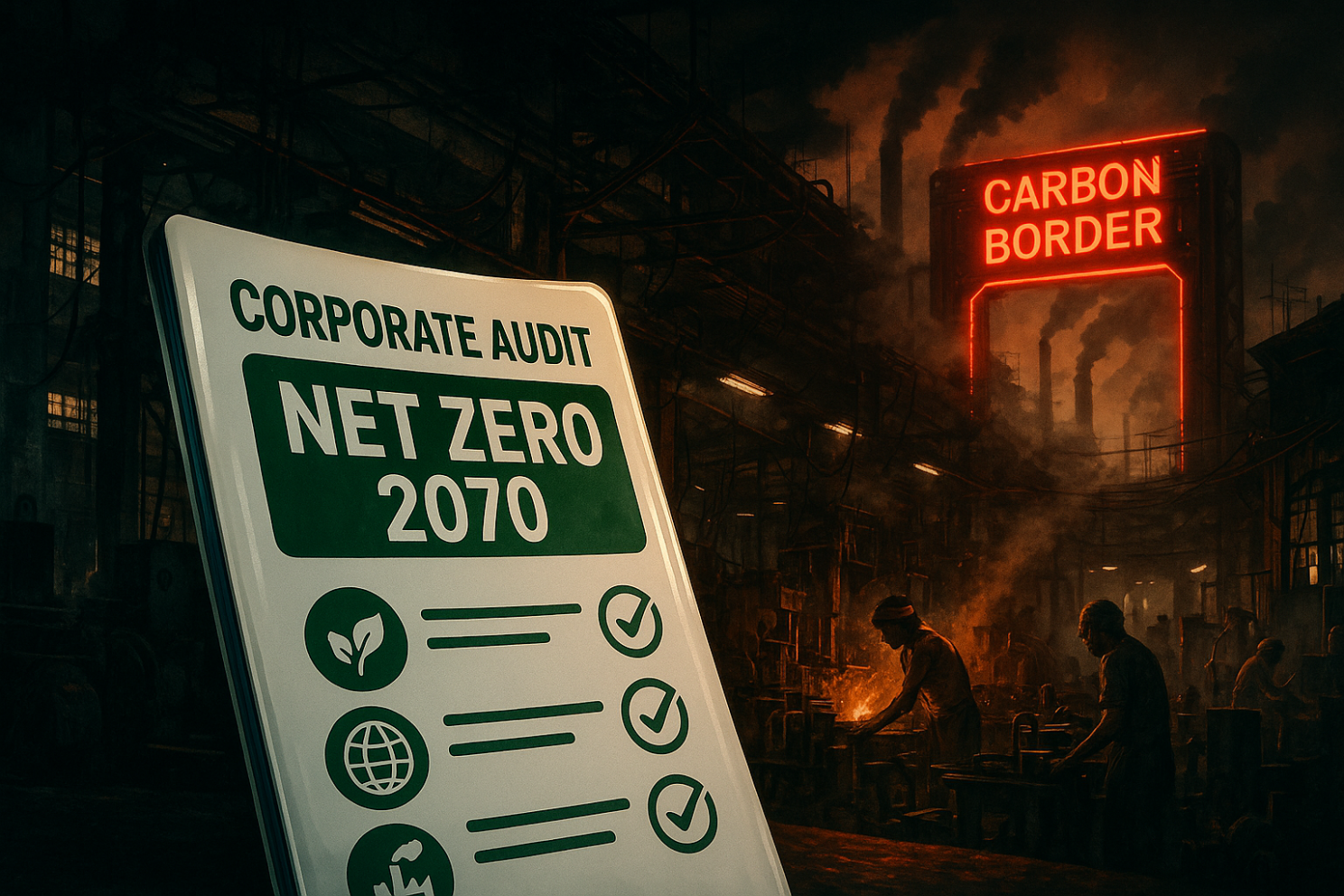

Reality Check #1: The Compliance Illusion

Every second panel discussion talks about “sustainable manufacturing.” Yet on the ground:

- Less than 20% of Indian factories have baseline carbon data.

- Only a fraction can pass global audit standards for supply chains.

- “Net-zero by 2070” is the headline, but the next 7 years will decide who gets locked out of EU and US markets because of carbon-border tariffs.

The OECD report bluntly puts it: India’s infrastructure gaps, patchy R&D, and uneven energy access are bottlenecks that no amount of policy slogans can bypass.

Reality Check #2: The Economics Nobody Likes to Talk About

Green manufacturing isn’t just about technology. It’s about who pays the bill.

- Switching to renewable power? Costs 20–30% more in the short term.

- Water recycling or zero-discharge plants? Expensive upfront, benefits show up 5–7 years later.

- Verified carbon audits and traceability? Another overhead SMEs can barely afford.

Here’s the brutal truth: domestic buyers rarely reward green premiums. So most firms will run a dual supply chain:

→Green for export (to pass EU/US gates).

→Brown for domestic (where cost still wins).

This split creates duplication, brand risk, and thinner margins. But for many, it’s survival.

Reality Check #3: Climate Costs Are Already Here

This isn’t theoretical. Factories in India already face:

- Flood risks in Chennai and Assam disrupting supply.

- Water stress in Rajasthan and Maharashtra killing textile and dye units.

- Heat waves reducing labor productivity and raising cooling costs.

Climate isn’t waiting for compliance deadlines. It’s already an unpriced overhead.

OECD Lens: What’s Urgent vs. Ignore

The OECD study highlights:

- Urgent: Infrastructure reliability (power, logistics, ports). Without this, no amount of “green branding” matters.

- Ignored: Productivity upgrades in MSMEs. Over 90% of Indian factories are small and mid-sized, and most don’t have the balance sheets for deep retrofits.

This is the blind spot. Policy loves big-ticket incentives (solar parks, EV subsidies), but the real battle is in Tier-2/Tier-3 factories that form the backbone of supply chains.

What Founders & Operators Should Actually Do

Forget the grand speeches. Here’s what matters in the next 5 years:

- Start with the meter, not the manifesto. Know your real energy, water, and waste numbers. No data = no deals.

- Pick one wedge, not the whole pie. Retrofitting one boiler or one pump pays off faster than waiting for 100% renewables.

- Build climate trust infrastructure. Carbon audits, verifiable supply data, and IoT-based monitoring will become the real entry barrier.

- Collaborate horizontally. MSMEs can’t do this alone. Shared waste plants, pooled solar, joint audits → cheaper together.

- Accept that green ≠ free. Green isn’t a PR exercise. It’s an economic moat that costs upfront but protects long-term markets

The Takeaway: Green Won’t Win by Default

The future of Indian manufacturing won’t be decided by slogans like “Make in India” or “Net Zero 2070.”

It will be decided in shop floors, small towns, and mid-sized factories where every rupee is weighed.

Those who treat sustainability as compliance overhead will be left behind. Those who treat it as competitive edge will own the next decade.

Because here’s the hard truth: India can’t export its way to $1T manufacturing without importing sustainability into its DNA.

Frequently Asked Questions

Everything you need to know about the onboarding pipeline and data protocols